ENTSO-E's Warning: The Next Wave of Data Centers Cannot Wait for the Grid to Catch Up

Data centres are no longer "niche demand." They are now a systemic risk and a multibillion-euro opportunity for those who can read the numbers.

[DEEP DIVE]

On 15 May 2026, ENTSO-E, the European Network of Transmission System Operators for Electricity, of which Portugal’s REN is a member, published the most important document in years on the intersection between digital infrastructure and the power grid.

It is titled “Data centres and the power system: expected trends, challenges and opportunities.” Twenty-nine pages of technical analysis converge on a single, unambiguous conclusion: Europe’s power system is not yet ready for what is coming.

This is not alarmism. It is the recognition that data centres have undergone a structural mutation from small and medium-sized facilities into industrial assets whose consumption exceeds that of traditional heavy industry, and whose electrical behaviour challenges every assumption on which transmission grids were built.

The numbers and data behind the report

Let us start with the facts. Europe today hosts over 10,500 data centres with at least 50 kW of IT power. Total installed capacity stands at approximately 12.7 GW of IT power supply, of which 9.9 GW is in the EU27.

If 12.7 GW already feels substantial, what comes next is alarming:

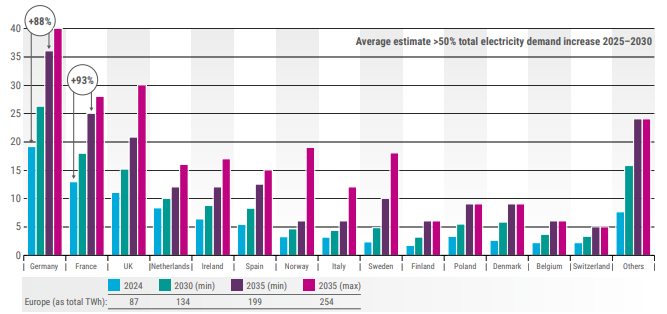

European data centre electricity demand is expected to grow by more than 50% between 2025 and 2030.

Total consumption will rise from 87 TWh in 2024 to 134 TWh by 2030 (minimum scenario), potentially reaching 254 TWh by 2035 in the maximum scenario.

The EU Cloud and AI Development Act, expected later in 2026, aims to triple installed data centre capacity in the EU within the next five to seven years.

To put these figures in perspective: 254 TWh represents roughly 10% of Europe’s current total electricity consumption. We are talking about creating, from near-zero, a demand load equivalent to the annual electricity consumption of Spain.

Growth is not evenly distributed. About 70% of the IT load increase will come from colocation facilities, and of these, 60 to 70% will be leased to hyperscalers (Microsoft, Google, AWS, and their peers). The “scale colocation” category — colocation facilities exceeding 50 MW, is growing at 30% per year.

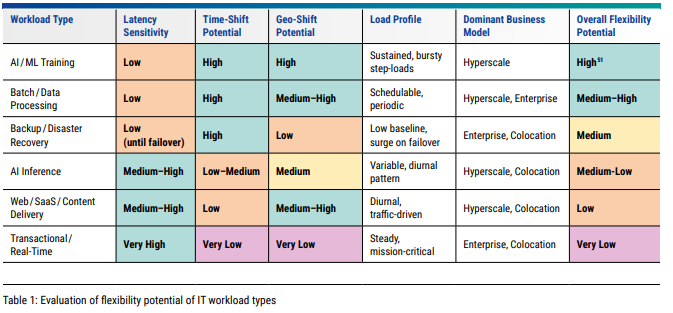

Data Centre Types

› Colocation and service provider data centres: These facilities lease space, power, and connectivity to customers who own and operate their IT equipment. Revenue for the colocation provider derives from leasing physical capacity rather than computing services. The critical feature from a grid perspective is the split-responsibility model: the colocation provider controls the facilities but not the workloads, creating a structural barrier to flexibility. Large “scale colocation” facilities exceeding 50 MW are increasingly leased to hyperscale tenants, blurring the boundary between data centres categories.

› Hyperscale data centres: These are massive facilities frequently exceeding 50 MW of IT power. These data centres are operated by major technology companies like cloud service providers, as well as large softwareas-a-service (SaaS) and internet platforms companies. They use scalable, highly efficient infrastructure to support cloud services, web hosting and, increasingly, AI services.

› Enterprise data centres: These facilities are owned and operated by a single organisation for its own use, typically banks, government agencies, or enterprises with sensitive workloads. These data centres are cost generators rather than profit drivers, and their workloads are tightly tied to internal business processes.

The Problem Is Not (Only) How Much Energy They Consume

Up to this point, everything could be solved with more generation. The real issue is how data centres consume electricity. And this is the point the ENTSO-E report dismantles with surgical precision.

The electrical architecture of a modern data centre is dominated by UPS (Uninterruptible Power Supply) systems. These systems are the interface between the grid and the IT load. Their primary function is to protect servers worth hundreds of millions of euros — and they do so with an unforgiving logic: at the slightest sign of grid disturbance (a voltage dip, a frequency variation), the UPS disconnects the load from the grid and switches to battery power.

What happens on the grid side? Hundreds of megawatts vanish instantaneously.

And then they come back. Reconnection is not standardised it can take seconds (power-electronic UPS) or hours (DRUPS). When the load returns, it does so as a demand shock that can depress grid frequency again, creating disconnect-reconnect cycles that ENTSO-E describes as “flapping.”

There are already documented incidents: load losses ranging from several hundred MW to over 1 GW following routine transmission faults. NERC, the North American reliability authority, has published specific incident reviews on the phenomenon.

But the problem begins before faults occur. Even during normal operation, AI workloads introduce load fluctuations that conventional monitoring systems cannot detect, let alone manage:

AI Training: power swings of 30 to 60% within milliseconds, as GPU clusters transition between computational phases. ENTSO-E classifies these as “load-driven disturbances” — active perturbations injected into the grid by the load itself.

Forced oscillations: Periodic load patterns from AI training can excite electromechanical modes of the power system, generating sub-synchronous oscillations that propagate across wide areas and are invisible to conventional SCADA systems. ENTSO-E explicitly recommends the use of Phasor Measurement Units (PMUs) with high-resolution sampling to identify and analyse these phenomena.

Translation: Europe’s transmission grids were built on the assumption that electricity demand is predictable, inertial, and passive. Modern data centres are the opposite of all three: programmable, instantaneous, and active.

Why Natural Gas Cannot Solve This Problem

The instinctive response from many decision-makers “if we need stability, we burn more gas” collides with an inescapable physical reality.

A combined-cycle gas turbine requires several minutes to start up and adjust its power output. Between the control signal and the mechanical response of the turbine, the timescale is measured in minutes, not milliseconds.

The load fluctuations caused by AI workloads occur in milliseconds. By the time the gas turbine begins to respond, the problem has already passed. Or, worse, it has already caused damage: a voltage violation that tripped protections elsewhere on the grid, an oscillation that propagated to a neighbouring control area, a frequency dip that caused another data centre to disconnect — and the cascade continues.

The physics is clear: grid stability with high penetration of dynamic digital loads requires resources with compatible response times. And those resources are not turbines. They are systems with power electronics batteries.

BESS as a Systemic Response

This is where Battery Energy Storage Systems (BESS) enter the equation — and the ENTSO-E report devotes an entire chapter (Chapter 5) to exploring them in the context of flexibility opportunities.

The technical case works across three layers:

1. Millisecond response

Batteries, through their inverters, can respond to control signals in less than one grid cycle (<20 ms). This means a BESS can absorb a load spike or inject power before voltage or frequency destabilise, something physically impossible for any thermal plant.

2. Control precision

A BESS response is digitally controlled, enabling power injection/absorption profiles that precisely track the dynamics of software-driven loads. ENTSO-E dedicates an entire section (5.3 — “From Grid-Safe to Grid-Supporting”) to showing how the same control capabilities a data centre needs for safe operation can be extended to provide grid services.

3. Integration with existing UPS architecture

The report highlights a critical economic advantage: adding battery capacity to an already-installed UPS architecture involves significantly lower CAPEX than a standalone BESS. The converters, protection systems, and grid connection hardware already exist only the battery modules need to be added (sources: ABB, PowerExchanger, 2022; Socomec, 2026; Saft, 2026).

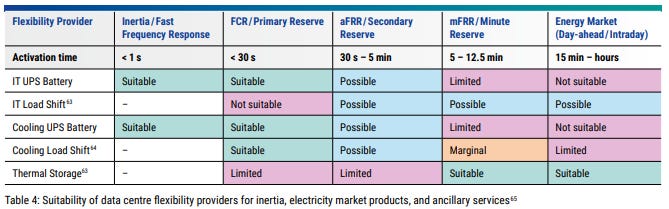

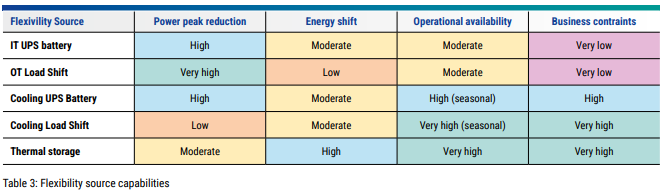

The ENTSO-E numbers for the technical flexibility that data centres can provide are striking:

Total technical potential across five European markets (Germany, Ireland, the Netherlands, Norway, and the United Kingdom): 16.9 GW by 2030.

Realistically available potential (after accounting for operational constraints and participation willingness): 3.8 GW.

Europe’s short-duration and ramping flexibility requirements are projected to roughly double by 2030, reaching an effective need of 15 to 30 GW.

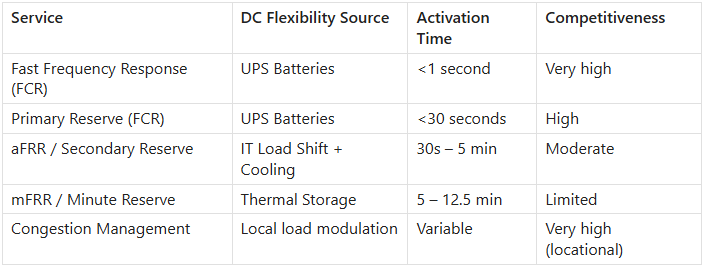

In market terms, the mapping is direct:

ENTSO-E is particularly clear on the locational value: in metropolitan clusters where data centres are concentrated (FLAP-D: Frankfurt, London, Amsterdam, Paris, Dublin), congestion management through load modulation and local generation is highly valuable and difficult to replicate with other technologies.

The Grid Bottleneck and Portugal’s Window

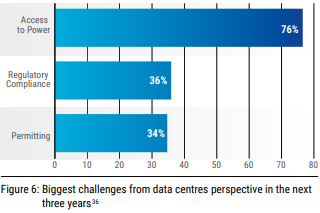

The grid-side numbers are equally stark. According to the report, drawing on EUDCA data (State of European Data Centres 2025), 76% of data centre operators identify access to electricity as their biggest challenge for the next three years well ahead of regulatory compliance (36%) and permitting (34%).

In the FLAP-D zones, connection waiting times range from several years to over a decade. Germany, Ireland, and the Netherlands are under particular pressure:

Ireland: TSO EirGrid published a resource adequacy assessment in December 2025 showing generation deficit risks as early as the 2026–2035 horizon. The CRU (Irish regulator) now requires new data centres to provide 100% on-site generation capacity plus 80% new renewable generation to cover their energy needs.

Denmark: TSO Energinet announced a temporary pause on new connections in March 2026 after receiving connection requests exceeding 60 GW for a national peak demand of just 7.3 GW.

Netherlands: Grid constraints across the entire Amsterdam region, with TSO TenneT declaring zero hosting capacity for new large loads at multiple substations.

And Portugal? Portugal has available grid capacity. It has abundant renewables (80%+ of the generation mix in April 2026, with Spain surpassing 50 GW of installed PV capacity). It has international connectivity. It has an active National Data Centre Plan (PNCD 2026–2027). And it has a geopolitical opportunity: while central Europe approaches saturation, the Iberian Peninsula is the natural expansion space.

But there is a real risk. As the report notes, submarine cables pass through Portugal, data passes through Portugal but the added value does not stay. Currently, the country largely serves as a transit point in the global connectivity infrastructure. The strategic question is: will Portugal remain a corridor, or will it become a destination?

The window is defined by the deployment speed itself. If the regulatory frameworks, flexible connection agreements, and business models are not ready when the next wave of hyperscale capacity looks for a location, that wave will go elsewhere.

Conditional Grid Connections for Consumption

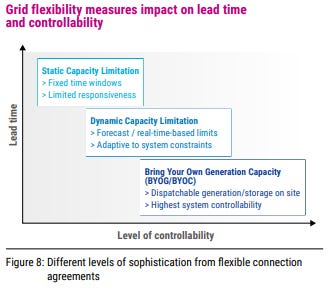

One of the most underappreciated instruments in the report is the concept of flexible connection agreements, which ENTSO-E addresses in Chapter 4 with concrete examples.

These agreements follow the same logic as conditional connection agreements already known in some markets for generation but oriented toward consumption. The modalities are progressive:

Static Capacity Limitation: The data centre accepts operation at limited power during predefined time windows.

Dynamic Capacity Limitation: Limits triggered dynamically by actual or forecast grid conditions.

Bring Your Own Generation (BYOG): The data centre contracts or builds dispatchable generation (renewables + BESS) to cover part of its demand outside the system.

The case study cited in the report is revealing: an analysis of a US data centre showed that combining flexibility and BYOG brought full operation forward by 3 to 5 years, with curtailment limited to 40–70 hours per year, equivalent to over 99% grid availability.

With BESS integrated into the UPS architecture and on-site renewable generation, a data centre can become a Virtual Power Plant (VPP), not only consuming energy but providing grid services (FCR, aFRR, congestion management) and participating in electricity markets.

The Urgency at the Heart of the Report

ENTSO-E closes the report with a warning that deserves to be quoted in full:

“The size and impact of data centres on grid planning and grid operation require a coordinated approach, under a broader framework of European and national authorities. The window of opportunity is defined by the speed of data centre deployment itself: the frameworks must be in place before the next wave of capacity reaches the grid, not after.”

There is a parallel here with what happened with solar PV in the Iberian Peninsula: for years, regulatory frameworks lagged behind technology. The result was zero and negative prices, massive renewable curtailment (20% of PV and 12% of wind generation in Spain in 2026), and projects at risk of financial default. Storage is now arriving to correct that imbalance — but the lesson is clear: regulation cannot arrive after the crisis.

With data centres, the window of anticipation still exists. But it is closing fast. The EU Cloud and AI Development Act, expected in 2026, could accelerate installed capacity by a factor of 3x. The report shows that the next wave of hyperscale capacity is currently in its location-decision phase.

Portugal: Corridor or Destination?

Portugal’s position on this chessboard depends on the choices made in the next 12 to 24 months. The country has genuine assets:

Available grid capacity in areas with abundant renewable resources.

Competitive electricity prices compared to central Europe, especially as levelised costs of solar-plus-storage continue to fall (IRENA: $54–82/MWh for solar + storage vs. >$100/MWh for new gas, forecast to fall below $50/MWh by 2035 in the best locations).

A dedicated national plan (PNCD 2026–2027) with AICEP as the single point of contact.

Elimination of the 7% generation tax (the “clawback” / competitive equilibrium mechanism), enacted by the Portuguese President in December 2025 — a clear competitive advantage over Spain, where this tax still applies and where the solar industry association UNEF classifies it as a “double charge” on storage.

But there are counterpoints. The same Iberian market that offers low wholesale prices also suffers from extreme solar cannibalisation (41.2% of all Spanish PV output in 2025 occurred during hours with negative prices, according to Pexapark). The Iberian transmission grid, while interconnected, has cross-border capacity limitations. And institutional coordination between Portugal and Spain, despite the recently announced Iberian Energy Observatory, remains far from the agility needed to respond at the speed of data centre investment.

Conclusion

The Two Transitions Must Move Together

The ENTSO-E report is, at its core, a document about interdependence. The digital transition — AI, cloud computing, big data — cannot advance without the power grid. And the energy transition — decarbonisation, flexibility, 24/7 renewables needs the demand and the control resources that data centres can provide.

The bridge between the two is storage. BESS co-located with data centres for dynamic stability. BESS along the transmission and distribution network for grid flexibility. Flexible connection agreements to close the time-to-power gap. Business models that transform an energy cost centre into a revenue-generating grid asset.

The question that lingers from the report is simple. Will Europe treat data centres as a grid problem to be managed or as the next major asset in the power system?

The answer determines who wins and who loses in the coming decade. And, right now, the window is still open.

🔗 The full ENTSO-E report is publicly available through the organisation’s official channels. Link in the comments.

This article draws on the ENTSO-E report “Data centres and the power system: expected trends, challenges and opportunities” (May 2026), as well as complementary data from the IEA, IRENA, EUDCA, Red Eléctrica de España, UNEF, APPA Renovables, and pv magazine.

Nice article. Very challenging situation. I have written my view here. https://substack.com/home/post/p-197885672

report ENTSO-E - https://eepublicdownloads.blob.core.windows.net/public-cdn-container/clean-documents/Reports/2026/FINAL_ENTSO-E_Data_Centres_260430.pdf